CDs offer a guaranteed return until maturity. To better gauge which CDs provide the better return, it helps to have a CD calculator. In this article, we will learn about CDs and how to select the most appropriate ones using a CD calculator.

What is a Certificate of Deposit (CD)?

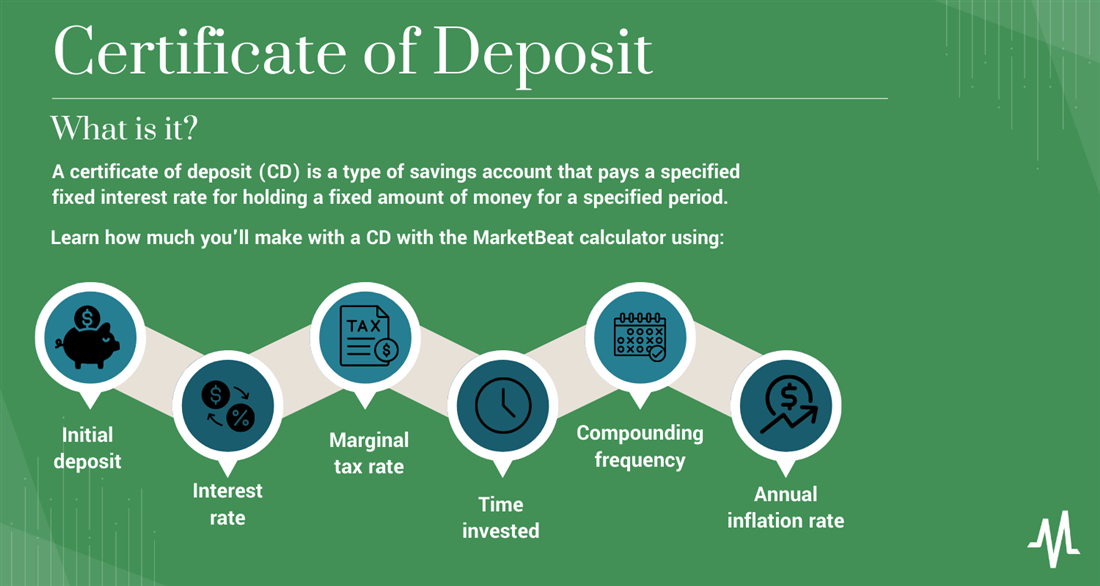

Banks and financial institutions offer CDs. A certificate of deposit (CD) is a type of savings account that pays a specified fixed interest rate for holding a fixed amount of money for a specified period. CDs pay a higher interest rate than regular savings accounts since CDs lock the money for fixed periods, ranging from months to years.

Longer-dated CDs pay a higher interest rate than shorter-dated CDs because the bank or financial institution has a longer time frame to invest the funds. CDs purchased through a federally insured (FDIC) bank are insured up to $250,000.

History of CDs

CDs were introduced in the U.S. during the 1920s. Banks would offer CDs to attract long-term deposits in exchange for a low-risk and secure investment from customers. They were initially offered only to institutions and high net-worth customers but eventually became more mainstream and available to the general public in the 1970s. The growth of the money market provided higher interest rates and abundantly more liquidity. This allowed banks to compete with each other to attract more deposits. Higher interest rates in the 1980s accelerated the popularity of CDs as they yielded more than savings and money market accounts.

CDs are sensitive to the U.S. Federal Reserve's interest rate policy. Rising interest rates mean higher interest for CDs and vice versa. CDs have guaranteed interest and provide the security of FDIC insurance, so depositors don't have to worry about their bank going under while holding their funds. Online banking has made CDs even more accessible to the general public.

Where and How to Purchase CDs

You can purchase CDs at commercial banks either through a local branch office or online. You can also purchase them at credit unions. These nonprofit financial cooperatives provide competitive interest rates and usually more flexible terms than commercial banks. Internet banks also sell CDs at usually better rates than commercial banks since they have less overhead without physical branch locations. Brokerage firms can offer a wide range of CDs beyond the traditional ones at your local bank. Purchasing a CD requires you to open an account with the financial institution. These are a type of savings account where money can be deposited but only withdrawn at maturity without facing a penalty.

How to Use CDs

You can use CDs for many purposes. While they offer a higher interest rate than regular savings or checking accounts, they are helpful for specific situations. Since they lock up your money for a fixed period, you can use them as an emergency fund. You would need a real emergency to risk paying a penalty fee to access the money.

CDs are also good savings instruments since you must leave the money and earn interest or potentially suffer an early withdrawal penalty. CDs help consumers avoid impulsively spending money. Since they pay a fixed interest rate, CDs can also serve as an income vehicle for retirees. CDs can help diversify your portfolio when looking to take risk off the table but still collect a guaranteed risk-free rate of return.

Withdrawing from a CD

CDs have fixed holding periods with a maturity date. For example, a one-year CD bought on February 1 would mature on February 1 of the following year. At the maturity date, you can withdraw your principal and interest to close out the CD or renew it at the current interest rate. Knowing how to calculate CD interest is vital to make the right decision.

Banks usually alert you that your CD is coming up on its maturity date, allowing you to withdraw or renew it. Banks provide a grace period from 10 to 14 days after maturity for customers to withdraw funds without getting hit with penalty fees. It's essential to understand the terms of the CD provided by the institution, as they can vary. Some institutions have an automatic renewal policy that renews the CD on the maturity date at the current interest rate. Other institutions may close out the CD and send a payment in the mail without further instructions to renew. The same applies to penalties for CDs. Some institutions will charge varying fees for penalties, while some forgo penalties for early withdrawal.

Types of CDs

Many types of CDs may or may not be available at your local bank or through various online financial institutions. Check directly with the institution and understand the terms before you purchase one type of CD over another.

Brokered CD

A brokered CD is purchased through and held at the brokerage. The brokerage is the middleman between the customer and the issuing institution. The CD stays in the customer's brokerage account. Brokered CDs are more flexible with various terms than traditional CDs. A broker can offer CDs from various financial institutions with a wide selection of terms to suit your situation. Similar to bonds, they can be bought and sold in the secondary market before they reach maturity.

However, brokerage CDs also carry more fees, including account maintenance fees. Calculating CD interest is prudent to determine which brokered CD is right for you.

Bump-Up CD

A bump-up CD enables you to increase or "bump up" the interest rate once during the investment period. You can use this option if you're still determining whether you want to stay at the same fixed rate for the whole term of the CD and risk missing out on possible interest rate hikes.

A bump-up CD removes that risk by allowing for a one-time bump up to current interest rates during the investment period. You pay for that flexibility — they start with a lower interest rate than traditional CDs.

Callable CD

A callable CD gives the issuing bank or financial institution the right but not the obligation to redeem the CD before its maturity date under certain conditions. Banks only call the CD when interest rates are falling, not rising. It protects the bank from paying a higher interest rate when interest rates go lower. Depositors receive their principal and the interest paid up to the time of redemption. These are less common than traditional CDs. Callable CDs come with both a maturity date and a callable date. The callable date is the bank's last day to call or close out the CD.

Liquid CD

A liquid CD enables the depositor to withdraw early without incurring penalty fees. These are also called non-penalty CDs. These CDs allow for more flexibility in an emergency where access to funds is critical. That flexibility comes at a cost since liquid CDs offer lower interest rates than traditional CDs. It's prudent to compare CDs once you learn how to calculate CD interest to make the best choice.

Traditional CD

A traditional CD is a savings product that provides a fixed interest rate for a fixed holding period on the money deposited with a maturity date. Traditional CDs have early withdrawal penalties to prevent the temptation to pull funds early. Traditional CDs are FDIC-insured up to $250,000. They are a low-risk, fixed-income investment. A CD rate calculator can be used to quantify how much interest would accrue for the CD term.

Zero-Coupon CD

A zero-coupon CD, or a deep discount CD, doesn't pay interest. You buy the CD at a discount and receive the total face value at maturity.

For example, you might buy a $10,000 five-year zero-coupon CD for $8,000, which would entitle you to receive the total $10,000 face value of the CD when it reaches maturity five years from the purchase date. This CD is best for risk-averse investors who only need to access funds for a short period. It is helpful to use a CD interest calculator to quantify the implied rate of return.

CD Laddering

CD laddering is a strategy that helps to diversify your CD holdings, enabling the flexibility of access to your money while optimizing the rate of return. It allows you to stagger your maturities so that you have access to your money without incurring penalties while still collecting interest.

If you want to give yourself the option to access some of your money yearly, you could ladder your CD maturities by purchasing a one-year, two-year, three-year, four-year and five-year CD. Laddering allows interest rates with longer-dated maturities to pay the higher interest rate. As CDs reach maturity, you can withdraw the funds or renew them again for a longer maturity with the current interest rate. This strategy provides access to some of your money while providing a steady stream of interest income.

How to Use the MarketBeat CD Calculator

You can use the MarketBeat CD calculator to help you figure out how much interest you will earn on a CD. To use it, you must input various information in the appropriate fields to receive the results.

- Initial deposit: How much are you going to invest in the CD? Enter in the amount of money you plan to invest.

- Interest rate or annual percentage rate (APY): What is the annual interest rate of the CD or the CD calculator APY? The interest rate is how much the financial institution will pay on the principal amount as a percentage per year. Annual percentage rate (APY) is the total amount of interest earned in a year, which also takes compounding into account.

- Marginal tax rate: What is your marginal income tax rate? Depending on your taxable income and filing status, this amount will range from 10% to 37%. You can find your marginal tax rate on the IRS website.

- Time invested: What is the duration of the CD? How long will your money stay in the CD?

- Compounding frequency: What is compounding frequency: daily, monthly, quarterly, semi-annually or annually? Compounding refers to calculating the interest earned on the principal amount and any previously earned interest. This is different from simple interest, which only calculates the interest on the principal amount and usually expressed as the annual percentage rate (APR). It doesn't calculate any previously earned interest. The frequency of compounding refers to how often the interest is calculated and added to the principal, the initial deposit. Monthly compounding means interest is calculated and added to the principal and previously earned interest on a monthly basis. Higher compounding frequency earns you more interest on a larger balance each time it compounds. You can find out the compounding frequency of a CD in the terms of the agreement. The more frequently the interest is compounded, the higher the APY will be.

- Annual inflation rate: What is the annual inflation rate? You can find it in the latest CPI monthly report from the U.S. Bureau of Labor Statistics.

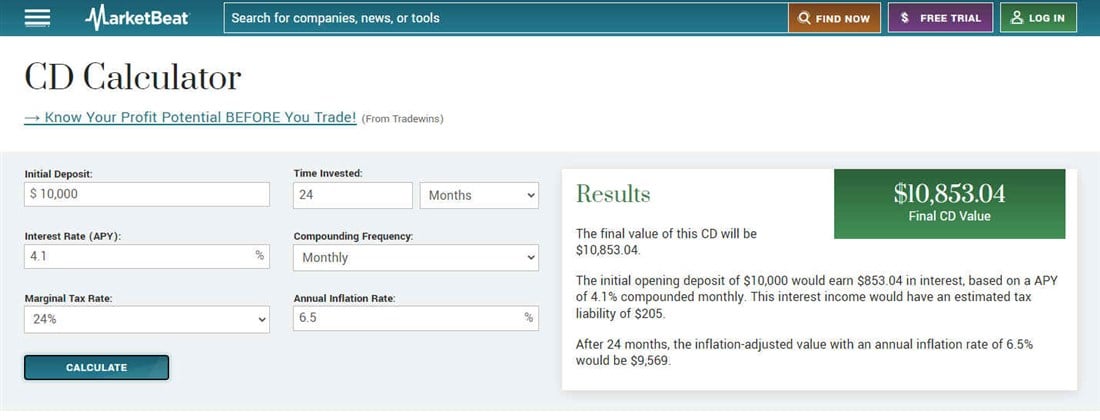

For example, let’s say you plan to deposit $10,000 in a CD, that you will have an interest rate of 4.1%, a marginal tax rate of 24%, a CD duration of 24 months, compounding monthly and with an inflation rate of 6.5%.

After you input this information, click “calculate.”

The results show that when the CD reaches its two-year maturity date, a $10,000 deposit will be worth $10,853.04. It would have a tax liability of $205. If you apply inflation to the results, the inflation-adjusted value would be $9,569.

Example of Using CDs

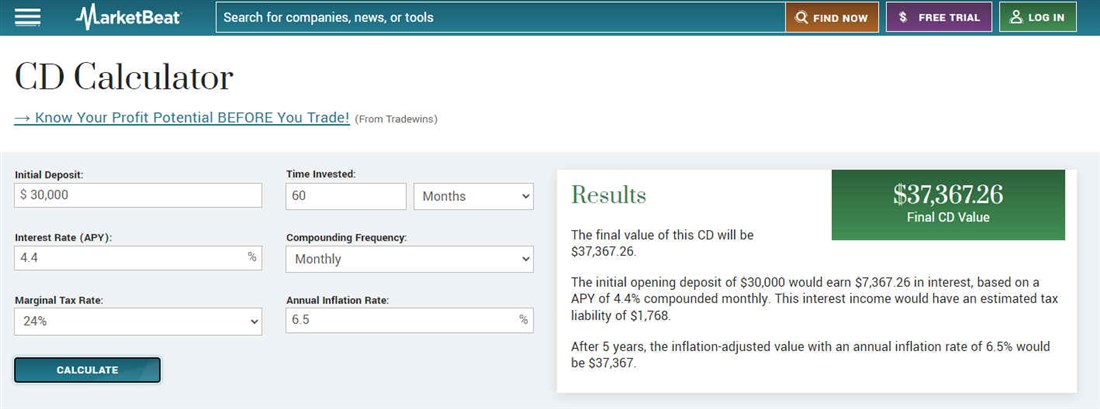

Let’s say you want a risk-free way to save up for your 13-year-old's college tuition and you have $30,000 ready to deposit today. You can use the MarketBeat CD calculator to determine how much you can earn risk-free on a CD.

In this case, with an initial deposit of $30,000, APY of 4.4%, monthly compounding frequency, 24% marginal tax rate and 6.5% annual inflation rate, the final value of the five-year $30,000 CD would be $37,357.26. The tax liability would be $1,768.

Shop and Compare CDs

With rising interest rates, commercial banks and financial institutions are all competing for deposits. Internet banks tend to offer the highest interest rates if you are comfortable with not being able to access a physical branch and talk to a person face to face. Keep a certificate of deposit calculator handy so you can comparison shop.

Ensure the financial institution you purchase a CD at is FDIC insured. Since $250,000 is the limit of FDIC insurance, be sure to cap your investment in any single CD to below $250,000. It's essential to find the frequency of compounding and not just assume it's monthly. A higher frequency of compounding means you’ll receive more interest income.

Position Your Portfolio with MarketBeat’s Calculators

MarketBeat provides a number of incredibly useful calculators for investors and traders. Use the MarketBeat dividends calculator to learn how much income your dividend stock portfolio can earn over time. Use the MarketBeat dividend yield calculator to compare dividend yields between different stocks. If you like to scale into stock positions, then the MarketBeat stock average calculator will help you calculate your average cost basis. Want to know how much profit you’ve made on a stock? Try the MarketBeat stock profit calculator. Use the MarketBeat stock splits calculator to see how a stock split announcement will affect your investment.

FAQs

Here are some frequently asked questions about CDs.

How much does a $10,000 CD make in a year?

How much interest a $10,000 CD makes in a year depends on the CD's annual percentage yield (APY) and the compounding frequency. If the bank offers 4% APY on a one-year CD that compounds annually, it will make $400.

How do you calculate a CD?

You can calculate the value of a one-year CD that compounds annually by multiplying your deposit amount by the APY. For a CD that compounds more frequently monthly, it's best to use the MarketBeat CD Calculator. A $10,000 deposit on a 4% APY one-year CD that compounds annually would earn $400 interest. However, the same CD that compounds every month would earn $407.42.

Can you get 6% on a CD?

Banks make their interest income from the difference between the federal funds rate and the APY offered on a CD. Therefore, a 6% APY on a CD would require a federal funds rate higher than 6%. A 6% CD is possible if the U.S. Federal Reserve continues to the federal funds rate higher than 6%.